Credit Scores Explained

If you feel as though your credit score is some sort of mysterious secret, then you are not alone.

While there is no verifiable statistic as to how many people feel this way, the fact that the credit reporting agencies don’t readily reveal their calculation methods makes easy to see why people are in the dark about what a good credit score should be.

You may not need to know the exact formula, but it’s still smart to understand how they come up with your credit score so you can whatever possible to maintain or improve your score.

After all, if you don’t know what goes into your credit score, there is no real way to do anything about it. Having a better idea of what elements go into determining it and how it’s calculated allows you to have more control over your financial health.

With that in mind, here is a breakdown of what the credit score is made of.

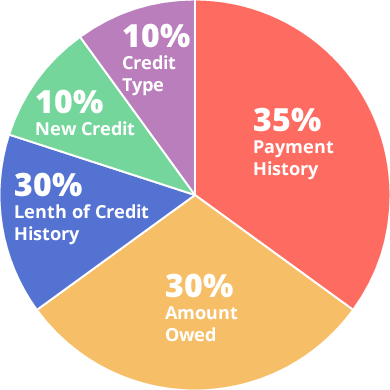

- The most important part of a good credit score is based on your history of making payments. Believe it or not, this counts for a staggering 35% of your overall credit score. Now, if you have a spotless record of making payments on time, then this is good news. However, if you occasionally forget to pay a bill and are routinely a few days late, then this could be bad news. I say ‘could be’ because different creditors have different policies on when they will report a late payment to the credit agencies. However, you don’t know what that threshold is, so it’s best to pay all your bills and loans on time.

- Your blend of credit adds up to 10% of your score. Having a mortgage, car loan, credit card and perhaps a store account that you pay on is a sign to the agencies that you can handle a variety of credit options. Be sure that you can handle all of them, though, as not paying on time on even one type can count against you.

- 15% of your credit score is determined by how long you have had a credit history. Of course, the better you have handled that credit over the years, the better it will be for your score. But it’s still better to have a more established credit record than a shorter one.

- Second in weight to your payment history is the total amount you owe. This factor accounts for 30% of your score. The total amount you owe is compared to your income in what’s known as the “debt to income” ratio. The lower, the better. You should aim to keep your total debt at 25% or less of your annual income to have the best effect on your rating.

- New inquiries into your credit are a warning sign that you may be overextending yourself and account for 10% of your total score. The one exception is if you are the one looking at your credit report.

As you can see, there is no real mystery when it comes to your credit score breakdown. Knowing how much weight is given to each portion of your score can help you decide where to first focus your efforts when you start trying to improve your credit score.

Good Credit Score Number

Here’s a quick question: What is the average U.S. credit score? The answer is 703. The average FICO® Score* in the U.S. is 703 according to data from Experian from the second quarter of 2019. So, how close did you get? If you were far off, that’s okay. Before you can make an accurate guess, you need to know a few things. You need to have some idea of how the economy is doing. You also need to know what the full range of credit scores is.

On the first point, a declining economy can harm credit scores.

However, as of now the downturn in the economy has not had as much of an impact…yet. None the less, it could still affect credit scores, so it makes sense to do what you can to maintain or improve your score, despite a sluggish economy.

The range for FICO credit scores is between 850-300. A perfect score is 850, and the worst possible score is 300. A bit of quick math tells us that the average of those two numbers is 575. That’s what the math tells us, but the national average credit score is now 703.

This is mostly because no matter how tough things get, people still do their best to pay their bills, and pay them on time. Whatever the reason, the actual average of 703 is significantly higher than 575.

More confusion is added by lenders who do not disclose what the cut-off point is for different terms of loans. Not to mention that these points can change at any time, and for a variety of reasons.

For example, while you may have had an easy time getting a good loan with a credit rating of 680 (10 points below average) just three years ago, it would be very difficult to get those same terms today.

So, what kind of score do you usually need to get the best terms today? Again, each lender is different, but overall you will need a good credit score number of 720 or better to make sure you will get the best terms. That’s quite a leap from 703, and 17 points above average.

Lenders may have more stringent standards because the economy is affecting them as well, or it could be because they see everybody as a higher risk than they used to. Of course, the reason doesn’t matter if you can’t get the best terms for a loan, or if you can’t get a loan at all.

MBNA on their website states “What counts as a good credit score, varies between the UK’s consumer credit reference agencies. The main ones, Experian, Equifax and TransUnion, all have their own scoring systems. For Experian, anything over 881 is classed as good or excellent. For Equifax it’s anything above 420, and for TransUnion it’s 4 and over.”

You should also know that each state has its average credit score. This means lenders have different numbers to work with in each area.

As an increasing number of people are finding out, you must be very careful when dealing with credit cards. One of the things that makes it so easy with credit card is that they are so convenient and safe to use. In many ways they are better than cash, especially if your purse or wallet is stolen.

Also, many things require the use of credit cards. In short, they are close to a necessity in today’s economy. However, all their benefits come at a potential cost. Even the most careful consumers can quickly find themselves in trouble, due to no fault of their own.

Related articles:

How to Avoid Financial Crisis and Prepare for the Coronavirus Outbreak

Credit Reports Matters

One of the most important thing you can do regularly is to check your credit reports, at least yearly. Make sure you get one from each of the three major credit bureaus: Experian, Equifax, and Trans Union. Don’t assume that the information will be the same on each one, it won’t be. Checking your credit report matters.

If you discover a mistake contact that bureau immediately in writing with any documentation you need to back up your claim that a mistake has been made. The credit bureau has to make the corrections to your credit report within 30 days which can result in an almost immediate boost in your credit score.

Since it can often take much more than 30 days to get a desirable credit score you should start now. Don’t wait until a few months before you want to apply for that new car loan or a new mortgage. If you go into your local bank with a strong credit score you will not only have a much easier time of being approved, you will also qualify for much, much better interest rates which can save you big bucks throughout the loan. It will also make your monthly payments smaller and easier to handle.

If you choose to hire someone to help you with your credit history repair just make sure that you are careful who you choose. Take time to read the fine print and find out what, if any, the charges will be to you for the help. Sometimes a loan consolidation may be a good option, sometimes not, ask questions so you can make the best decision for you.

There are three major credit bureaus (also called credit reporting agencies or CRAs):

- Equifax – www.equifax.com

- Experian – www.experian.com

- Trans Union – www.transunion.com

Apart from collecting financial data on virtually everybody. Each of them also are responsible for generating a credit score. So, there is the full-blown credit report which lists all of your creditors, how often you pay, what you owe, and so on. This part of it can fill up page after page of data. Then there is the credit score. This is a single number that attempts to encapsulate the entire report into an objective score that applies equally to everybody.

When it comes right down to it, the three big credit agencies are responsible for the information that is shared with those who request access to your credit report. In turn, your creditors will use that information to decide what terms they will offer you. To put it bluntly, these credit score companies have a lot of power when it comes to American consumers. For this reason, it’s a good idea to do your best to maintain a good credit rating and fixing any errors on your report.

Related article: How To Budget For Financial Independence

Good Credit Score

While it’s a serious thing, and can have a big impact on your life, it’s relatively easy to understand the basics of getting a good credit score. Here’s what you need to know.

The most important thing you can do for your credit score is to religiously pay all of your bills on time. As soon as you get credit or another loan, start making the payments right away. you may even want to make them a few days early to ensure they will be processed on time.

You should pay the full balance of any bills that require it (such as telephone and utilities), and at least make the minimum payment on those bills that are intended to carry a balance. Pay as much over the minimum whenever possible. Your payment history accounts for the largest part of your credit score, so don’t take it lightly.

After making all of your payments on time, the next best thing to do is to spend less than you earn. This extends to not buying things that are too expensive. When purchasing credit, do not look at the monthly payment, but what the total cost to you will be.

A common mistake is to see something you can’t afford, say a $5000 hot tub, then calculate the monthly payment. You may be thinking you can afford $200 a month, but not the $5000. Be careful! That $200 month is probably for 4 years, and that adds up to $9600! Surely, if you can’t afford a $5000 hot tub, you can’t afford to spend nearly twice as much on it. Living within your means will also keep your debt-to-income ratio lower, which is also good for your credit score.

The final thing you can do is get a copy of your credit report from each of the big three credit reporting agencies regularly. Check for any errors and report them right away. If the agency finds you are correct, they will remove the mistake from your report. You have to check all three as not all creditors use all three agencies. Each one will have slightly differing records, and it’s best to be thorough.